IFSEC Insider is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Security market analysts from Omdia have highlighted the potential growth of an integrated Physical Security as a Service system – one that combines both Access Control and Video Surveillance as a Service solutions. Ivy Sun, Senior Analyst, Physical Security and Bryan Montany, Senior Analyst, Physical Security, provide insight into the benefits, opportunities and potential barriers to adoption.

An integrated Physical Security as a Service (PSaaS) system takes the outsourcing of security software to the cloud one step beyond the traditional architectural framework of Access Control as a Service (ACaaS) and Video Surveillance as a Service (VSaaS) solutions. Integrated platforms that encompass both access control and video surveillance systems represent the future of cloud-based security, but these platforms will need the right solutions and innovations to drive growth.

Benefits of integrated Physical Security as a Service (PSaaS)

Omdia defines a fully integrated PSaaS system as a comprehensive security solution where customers pay on a weekly, monthly, or quarterly basis for a server that is capable of simultaneously administering an end user’s access control and video surveillance domains through a single interconnected database.

Fully integrated VSaaS and ACaaS solutions offer numerous advantages to end users, systems integrators and software vendors. From the end user’s perspective, acquiring a single PSaaS solution can be less expensive than investing in separate VSaaS and ACaaS systems. Integrated PSaaS solutions provide the most savings for owners of small and mid-sized facilities, and these end users are already more predisposed to invest in cloud-based security solutions.

An integrated PSaaS solution combines ACaaS and VSaaS functions in a single software offering, allowing security professionals to subsequently manage both systems through a single application. In addition, the consolidation of both video surveillance and access control data allows for more use cases of ‘big data’ analytics and greater opportunities to streamline automated security processes such as systems testing and maintenance tracking. The ‘big data’ analytics enabled through integrated PSaaS solutions can also be used by facility owners to assess occupancy levels of buildings with greater accuracy, remotely view attempted entries and confirm unauthorised security breaches in real time.

Want to know more about the security market for the UK? Download our exclusive report, written by the Omdia analyst team, to find out all you need to know!

From the perspective of systems integrators, an integrated PSaaS solution establishes a relationship between themselves and the end user, and they become responsible for managing and maintaining both the VSaaS and ACaaS systems. This streamlines maintenance routines and reports across both domains. Finally, VSaaS and ACaaS software vendors who can offer integrated PSaaS solutions can differentiate themselves from their competitors through a unified security management product offering. Most VSaaS and ACaaS vendors today are not currently able to offer integrated PSaaS solutions due to the major differences in the sales models, customer bases and hardware installed across each domain.

Integrated PSaaS: Market size and forecast

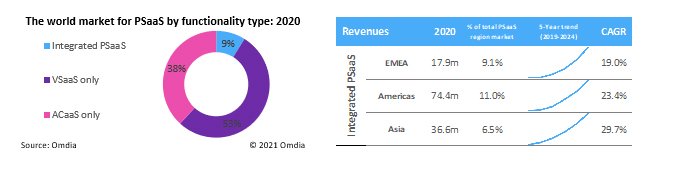

Despite the numerous advantages that integrated PSaaS systems offer, most PSaaS product offerings have focused on limited convergence through common user interfaces and the transmissibility of data between distinct ACaaS and VSaaS solutions. Omdia forecasts that the world PsaaS market is estimated to be worth $1.5 billion in 2020, but integrated PSaaS solutions were estimated to comprise less than 9% of the total PSaaS market. This percentage is only expected to grow to 13% by 2024. The market for integrated PSaaS solutions will grow at an impressive 24.6% CAGR over the next five years, but demand for these platforms will not displace the established VSaaS and ACaaS markets.

Barriers to adopting integrated PSaaS solutions

Several factors have prevented integrated PSaaS solutions from gaining more traction. The most crucial barrier that has limited growth is the challenge of combining unique ACaaS and VSaaS sales models into a single product offering.

Today, most ACaaS solutions are offered to end users through a sales model that calculates monthly fees based on the number of electrified doors in each facility with installed ACaaS equipment. This sales model encompassed nearly 90% of global ACaaS revenues in 2020. Billing per door is the dominant billing type for ACaaS solutions because this model allows for greater flexibility and scalability of services during the lifetime of a contract. These contracts can be easily modified to accommodate more or fewer electrified entryways depending upon the immediate needs of an end user. The per door model is easiest to monetise and generally supports a higher retention rate for end users when ACaaS contracts are renegotiated or renewed.

Most VSaaS solutions are built on sales models that revolve around the number of security cameras installed in a building. Early attempts by integrated PSaaS vendors to combine aspects of these approaches into a hybridised sales model have frequently been rejected by end users as too complex. Alternative methods to simplify these sales models with standardised charges are viewed as inflexible and incapable of adapting to rapidly changing security needs.

Another major barrier is a lack of education among end users regarding the potential benefits that integrated PSaaS solutions can offer. According to multiple vendors, most of the analytical functionality present in existing ACaaS and VSaaS applications are not properly used by their existing customer base. Many security professionals are either totally unaware of the potential benefits or are disinclined to accept any changes to their outdated security procedures. Many end users also distrust artificial intelligence, especially when AI is hosted on remote cloud-based servers and prefer to avoid any reliance on automated procedures to track threats such as suspected security breaches. Integration of ACaaS and VSaaS platforms may offer little additional value to these end users.

A final issue is the regional differentiations between market demand for ACaaS and VSaaS solutions. In 2020, more than 70% of the total ACaaS market was based in North America. By contrast, nearly two thirds of the total market for VSaaS solutions derived from sales in the Asia Pacific region, with most of those revenues stemming from the Chinese market. Communications providers such as China Telecom and China Unicom were estimated to be the largest providers of branded VSaaS solutions in China due to their relationships with the Chinese government. These companies have generally not expanded their offerings to include ACaaS functionality due to low demand from institutional end users in China.

The Chinese ACaaS market is expected to remain immature over the next five years, with opportunities disproportionately originating from multinational corporations in major metropolitan areas such as Beijing and Shanghai.

Opportunities for integrated PSaaS vendors

More opportunities for integrated PSaaS vendors have emerged in North America and Western Europe, where an increasing percentage of VSaaS and ACaaS providers have attempted to acquire or merge with vendors who could complement their existing offerings and round out their security portfolios. For example, Dean Drako, the CEO of video surveillance provider Eagle Eye Networks, acquired leading ACaaS vendor Brivo in 2015, in a move which enabled the two – though continuing to operate as separate entities – to combine solutions for a “unified cloud-based access control and video surveillance system”. Other VSaaS providers such as Arcules have focused on the organic expansion of their VSaaS offerings and have gradually introduced ACaaS features and functionality.

While integrated PSaaS solutions will comprise a minority of the total ACaaS and VSaaS markets over the next decade, innovative vendors can take steps now to overcome the barriers with their product offerings and distinguish themselves from competitors.

To combat aversion to PSaaS integration, vendors must appeal to the increasing percentage of stakeholders for ACaaS and VSaaS systems that are outside the conventional security domains. Managers, HR teams, IT professionals, and property management teams are becoming increasingly involved in day-to-day security operations and these stakeholders are more likely to appreciate the analytics provided and additional functionality enabled through PSaaS integration.

In addition, vendors must educate both resellers and end users regarding the features and prospective benefits of ‘big data’ analytics to save on operational costs, reduce the size of security staff and streamline processes such as credentialing and investigations of breaches. Finally, vendors must continue to innovate their sales models to provide embrace flexible and individualized, case-driven approaches to end users in different vertical markets.

Physical Security as a Service (PSaaS) report

The 2021 edition of Omdia’s Physical Security as a Service (PSaaS) report provides an in-depth analysis of convergence in the PSaaS market and includes market estimates and forecasts for both ACaaS and VSaaS revenues. This report analyses the significant trends, threats and opportunities for growth affecting the PSaaS market through 2024. Granular analysis is provided for both ACaaS and VSaaS market conditions by segmentations including solution type, billing type, and end user sector.

Bringing decades of high level research experience, Omdia’s portfolio includes dedicated security market analysts in a range of sectors, including video surveillance, access control, physical security, public safety & critical communications, smart buildings, and more. Find out more at Omdia’s dedicated physical security hub.

Keep up with the wireless access control market

Download this free report to find out more about:

The current state of wireless access control solutions in the market

The rising popularity of mobile access control

Awareness of cyber security regulations and how this relates to access control

The growing use of the cloud and ACaaS to manage access systems

How your choice of access control solution can impact sustainability

Integrated Physical Security as a Service platforms offer “great opportunities for innovative vendors”Market analysts from Omdia offer expertise on the market potential for integrated Physical Security as a Service applications.

Omdia

IFSEC Insider | Security and Fire News and Resources

Related Topics

Digging into Access Control as a Service – Misconceptions, nuances and challenges to wider adoption

ACRE announces Feenics and Matrix acquisitions

EBOOK: Access Control – Trends, Opportunities and Challenges

“the video surveillance provider Eagle Eye Networks acquired leading ACaaS vendor Brivo in 2015” this is false. The founder of Eagle Eye Networks Dean Drako acquired Brivo, Brivo and Eagle Eye are still separate companies. https://www.brivo.com/dean-drako-acquires-brivo-cloud-access-control-company-for-50-million/

Thank you for pointing this out – we’ve updated the piece.